Where Is the Market Heading

What the Stock Market Will Likely Do Until Election Day

How the Market Continues to Develop

As the Federal Reserve's recent 50-basis-point interest rate cut fades from immediate focus, the stock market could enter a period of relative stability leading up to the U.S. presidential election. Historically, calm periods on the macroeconomic front have often resulted in positive returns for stocks. According to a note from Bank of America analysts, "no news is good news" for stocks, and quiet weeks tend to yield better median returns than periods marked by economic disruptions or major announcements. Specifically, the median return during quiet weeks has been around +0.61%, compared to the typical +0.38% return in other weeks.

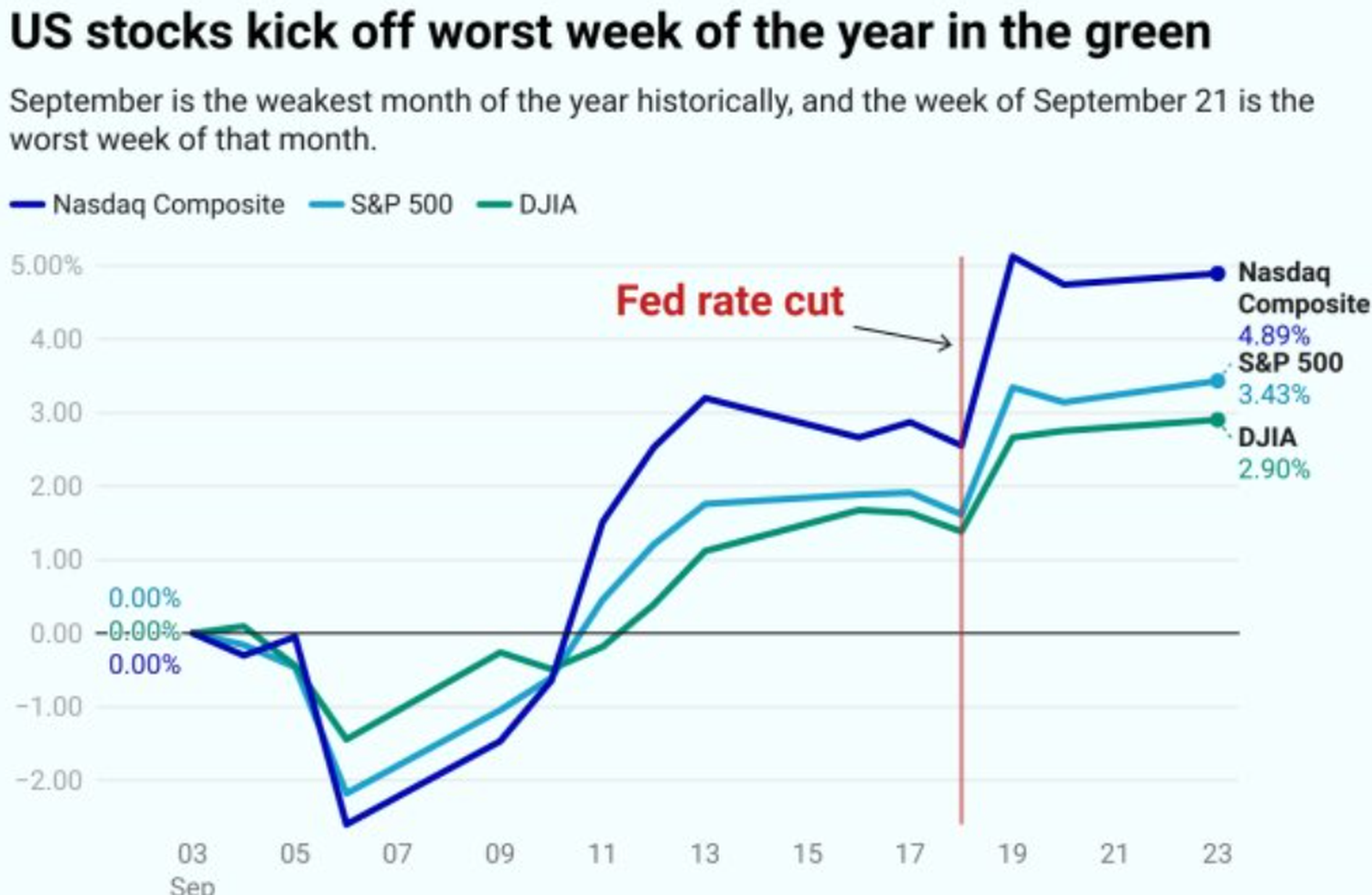

After the rate cut, both the Dow Jones Industrial Average and the S&P 500 reached record highs, signaling investor confidence. The performance during this time is notable because it came despite September historically being one of the worst-performing months for stocks. Investors were quick to celebrate the Fed's decision, pushing the major indices higher, even as some market analysts anticipated a more tepid reaction given past volatility during this time of year.

The Importance of Election Year Uncertainty

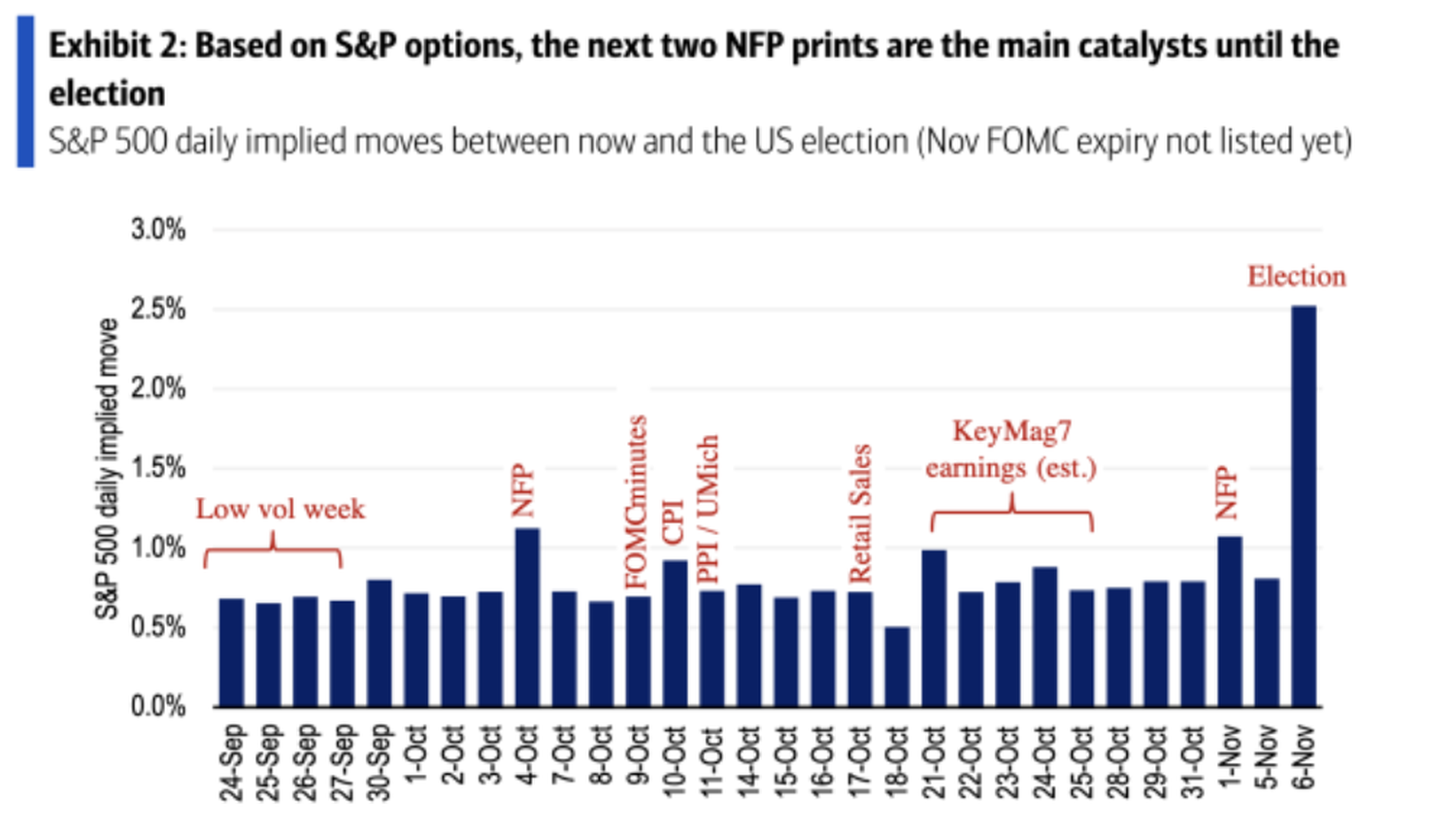

One major driver of volatility that lies ahead is the November 2024 election. As shown in the chart provided by Bank of America, the implied volatility—or the market’s expectation of future price fluctuations—rises sharply around election time. However, the weeks leading up to the election are likely to see less turbulence, with minor data releases such as inflation and employment reports causing only small ripples in trading activity.

Bank of America’s analysis also suggests that the market may "lean into the 'no news is good news' quip," meaning that the lack of disruptive developments should provide a supportive environment for equities in the short term. Though some bearish commentators are concerned about the broader economy and the risks of a recession, the market is currently benefitting from favorable conditions like low unemployment and steady economic growth.

Comparing Today’s Rate Cuts with Past Cycles

There is a bleaker perspective worth considering, especially when comparing today’s environment to past periods when the Fed initiated major rate cuts. Notably, in both 2001 and 2007, when the Fed launched rate-cut cycles similar to the one we're seeing today, the market was on shaky footing even before those cuts took place. Both periods were followed by significant stock market crashes—the dot-com bubble burst in 2001 and the Global Financial Crisis in 2007.

Despite these historical precedents, Jay Woods, Chief Global Strategist at Freedom Capital Markets, believes that while the market may experience some choppiness in the next month, the long-term outlook remains positive. According to Woods, over the next 3, 6, and 12 months, bulls (those who believe the market will rise) have historically won out. He highlighted that, following past initial Fed cuts, the S&P 500 has risen in 20 out of 20 instances one year later, with an average gain of 13.9%.

What to Expect in the Coming Weeks

Several factors will still have the potential to move the market before the election. Inflation reports and non-farm payrolls data are among the most closely watched indicators that could generate minor fluctuations. While these could create short-term volatility, they are unlikely to drive substantial changes in market sentiment unless the data is significantly worse than expected. For the most part, investors can expect a tepid trading environment until the election results start to loom larger in the market's focus.

However, election day itself could create substantial market volatility, as the results could shape future fiscal policy, including tax policies and government spending that directly impact corporate earnings. Investors should be prepared for sharper movements in the days surrounding the election, especially if the results are contested or unclear, which would increase uncertainty and potentially cause larger market swings.

Sector-Specific Recommendations

Bank of America is recommending that investors focus on rate-sensitive sectors during this period of relative calm. Specifically, they suggest overweighting financials, consumer discretionary, real estate, and utilities—sectors that tend to benefit when interest rates move or stabilize after a significant cut.

Financials: Banks and financial institutions can benefit from more favorable borrowing conditions as interest rates are cut. Lower rates can also support stronger consumer spending and borrowing activity, which boosts demand for financial services.

Consumer Discretionary: This sector, which includes companies in industries like retail, luxury goods, and leisure, tends to perform well when consumers have increased disposable income due to favorable economic conditions, such as those that could arise from rate cuts and government stimulus measures.

Real Estate: As interest rates decline, mortgage rates also drop, making real estate investments more attractive. Lower borrowing costs can lead to increased demand for homes and commercial properties, benefiting companies in this sector.

Utilities: Utility companies tend to offer stable dividends and have relatively low volatility. They can perform well in a low-interest-rate environment because investors often seek out steady income from dividends when bond yields are low.

Conclusion: The Likelihood of a Pre-Election Rally

As investors approach Election Day, the stock market could see a relatively calm and upward trend due to the lack of significant macroeconomic shocks. While some analysts point to historical periods when major rate cuts were followed by market crashes, others, like Jay Woods, remain optimistic about the long-term prospects of the market. Investors should expect a period of stability but should keep an eye on upcoming economic data and be prepared for potential volatility closer to the election.

Focusing on rate-sensitive sectors could provide opportunities for growth in the meantime, with financials, consumer discretionary, real estate, and utilities looking particularly attractive. As always, staying diversified and informed will be key to navigating the market as the election draws nearer.