Job Market Data and Federal Reserve Outlook

Wall Street Wobbles as Strong Jobs Data Adjusts Rate Cut Expectations

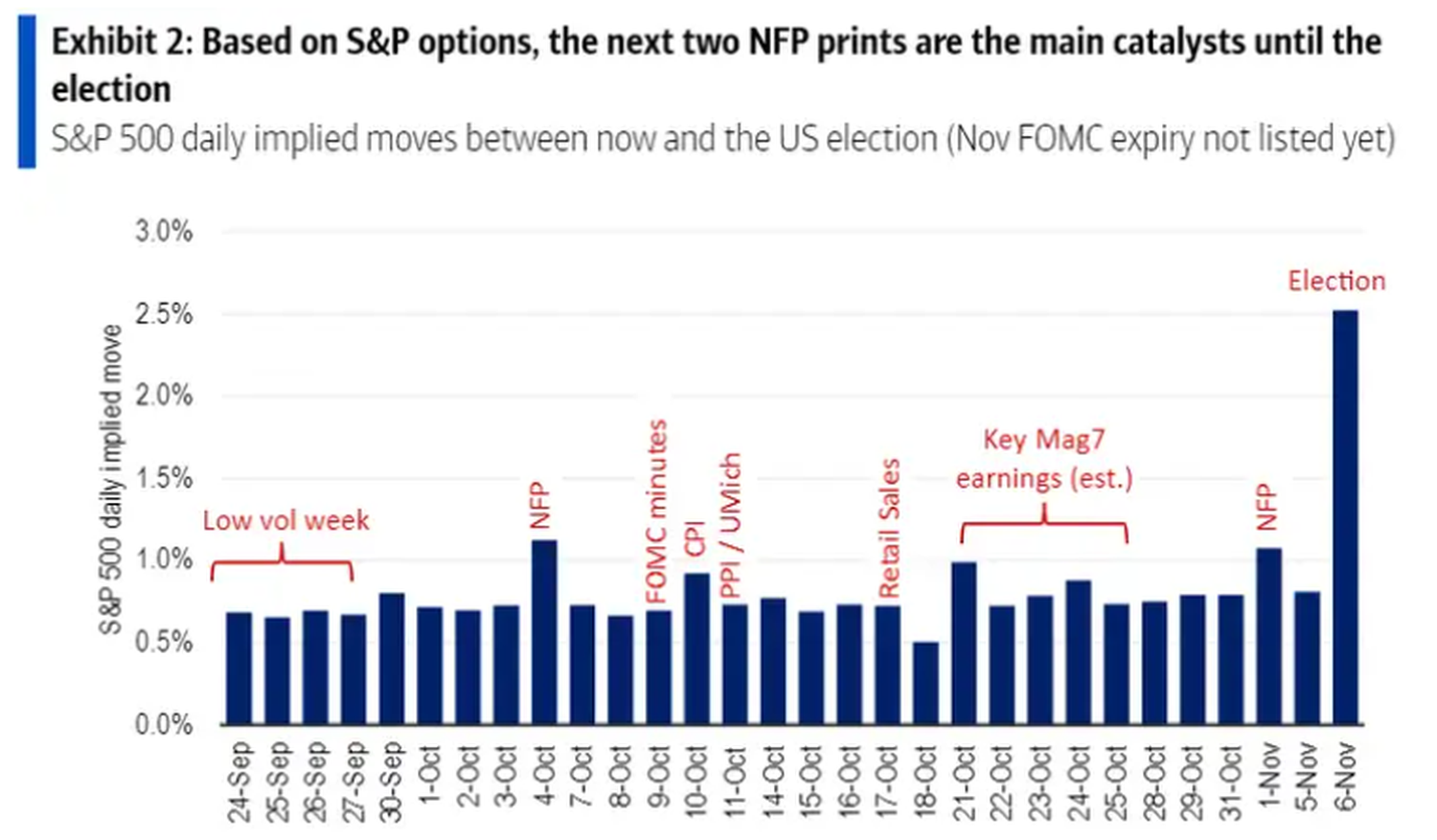

Key Dates and Market Catalysts

U.S. stocks saw mixed movements on Friday as the latest jobs report revealed unexpectedly strong growth in the labor market. The S&P 500 rose 0.4% midday, while the Nasdaq increased by 0.7%, buoyed by optimism over economic strength. However, the Dow Jones Industrial Average struggled to maintain early gains, reflecting a market adjusting to potential shifts in interest rate expectations.

The report showed that U.S. employers added 254,000 jobs in September, well above expectations. This news, while positive for the economy, has forced investors to reconsider how aggressively the Federal Reserve will cut interest rates going forward. Treasury yields surged, with the 2-year Treasury yield rising to 3.88% from 3.71%, as traders scaled back their predictions for further significant rate cuts.

Key Factors Driving the Market:

1. Oil Prices and Geopolitical Tensions:

- Middle East Conflict: The stock market has been reacting to rising geopolitical tensions, particularly concerns over Iran's potential missile attack on Israel. This is pushing oil prices higher, with Brent crude rising roughly 3% on Wednesday morning, surpassing $75 a barrel. While Israel is not a major oil producer, the involvement of Iran, a critical player in the global oil market, has raised concerns over broader supply disruptions in the region.

- Impact on Oil Stocks: U.S. oil-and-gas companies have benefited from the surge in crude prices. Notably, Exxon Mobil rose 2% Wednesday, continuing its strong week with a gain of 5.7%.

2. Corporate Earnings and Stock Movements:

- Nike: The athletic giant’s stock fell 7.8% despite beating profit expectations for the quarter. However, revenue came in below forecasts, and concerns over incoming CEO Elliott Hill's ability to reinvigorate the brand among consumers added pressure. Nike also withdrew its full-year financial outlook and delayed its investor conference.

- Humana: Shares of Humana dropped 20.5% after warning that a decline in its Medicare Advantage ratings could affect revenue in 2026. The company is contesting the Centers for Medicare and Medicaid Services' calculations.

- Tesla: The electric vehicle maker fell 5.8%, despite reporting a rise in vehicle deliveries. Investors may have expected a larger increase in deliveries, leading to a sell-off.

- Conagra Brands: Conagra, known for products like Duncan Hines and Reddi-wip, saw an 8.7% drop in stock after weaker-than-expected profit due to manufacturing issues at its Hebrew National brand during peak grilling season.

3. Job Market Data and Federal Reserve Outlook:

- Hiring Reports: The labor market remains under close watch as investors anticipate the official U.S. job market report coming on Friday. A recent ADP report showed that private employers hired more workers than expected last month, which could signal resilience in the job market.

- Fed Interest Rates: Traders are adjusting expectations for future Federal Reserve rate cuts, with many now anticipating a quarter-point cut, rather than a more aggressive half-point cut, based on current economic signals. Treasury yields rose in response, with the 10-year yield climbing to 3.81%.

Global Market Sentiment:

- China's Stimulus: Hong Kong’s Hang Seng index surged 6.2% as investors reacted positively to new stimulus measures by Beijing aimed at supporting the Chinese economy. Markets in China were closed for a holiday, but the uptick in Hong Kong suggests optimism regarding the effectiveness of these measures.

- Japan and Europe: The Nikkei 225 in Japan continued its volatile swings, dropping 2.2%, while European markets showed mixed results as investors assessed global risks.

Looking Ahead: Key Dates and Market Catalysts

Several major events are expected to shape market trends in the coming weeks as we approach critical political and economic milestones:

- U.S. Presidential Election: The race to the White House continues to loom large over markets, with investors keeping a close eye on potential policy shifts and their impacts on various sectors.

- Upcoming Economic Reports: The next major release is the U.S. employment report on Friday, which will provide more clarity on the state of the job market and could influence future Fed rate decisions.

- Corporate Earnings Season: Companies such as Lamb Weston (potato processing), McCormick (spices), and Cal-Maine Foods (egg production) are set to report earnings, with their results likely to add further volatility to the market.

Economic Winners and Losers

Sectors tied to economic growth, such as banking and travel, led the stock rally. Norwegian Cruise Line gained 5.8%, and JPMorgan Chase rose 1.8%, as investors anticipated these companies will benefit from a stronger economy. However, industries sensitive to interest rate changes, like homebuilding, faced headwinds. D.R. Horton, Lennar, and PulteGroup all fell at least 3%, reflecting concerns over higher borrowing costs.

Corporate earnings also played a significant role in the day’s movements. Nike dropped 7.8%, despite reporting stronger-than-expected profits, as investors were concerned about declining revenues and challenges ahead for the incoming CEO, Elliott Hill. Meanwhile, Humana plummeted 20.5% due to concerns over potential revenue losses linked to its Medicare Advantage ratings.

Oil Prices and Geopolitical Tensions

Crude oil prices saw a moderate increase on Friday, with Brent crude rising 0.7% to $78.17 per barrel. Although the market remains wary of potential supply disruptions caused by the ongoing conflict in the Middle East, Friday's gains were modest compared to earlier in the week. The rise in oil prices comes as global markets brace for Israel's response to the missile attack from Iran.

Conclusion

Friday’s trading session reflects a market in transition, as investors reassess economic strength and future monetary policy. The robust jobs report adds optimism for economic growth but complicates expectations for interest rate cuts. While sectors like banking and travel rallied on the positive economic outlook, rising Treasury yields weighed on housing and real estate stocks. Geopolitical tensions, especially in the Middle East, continue to pose risks to oil markets, adding further complexity to an already volatile trading environment.