Nvidia Earning Report

S&P 500 and Nasdaq Slip Amid Tech Weakness

How the Market is Developing

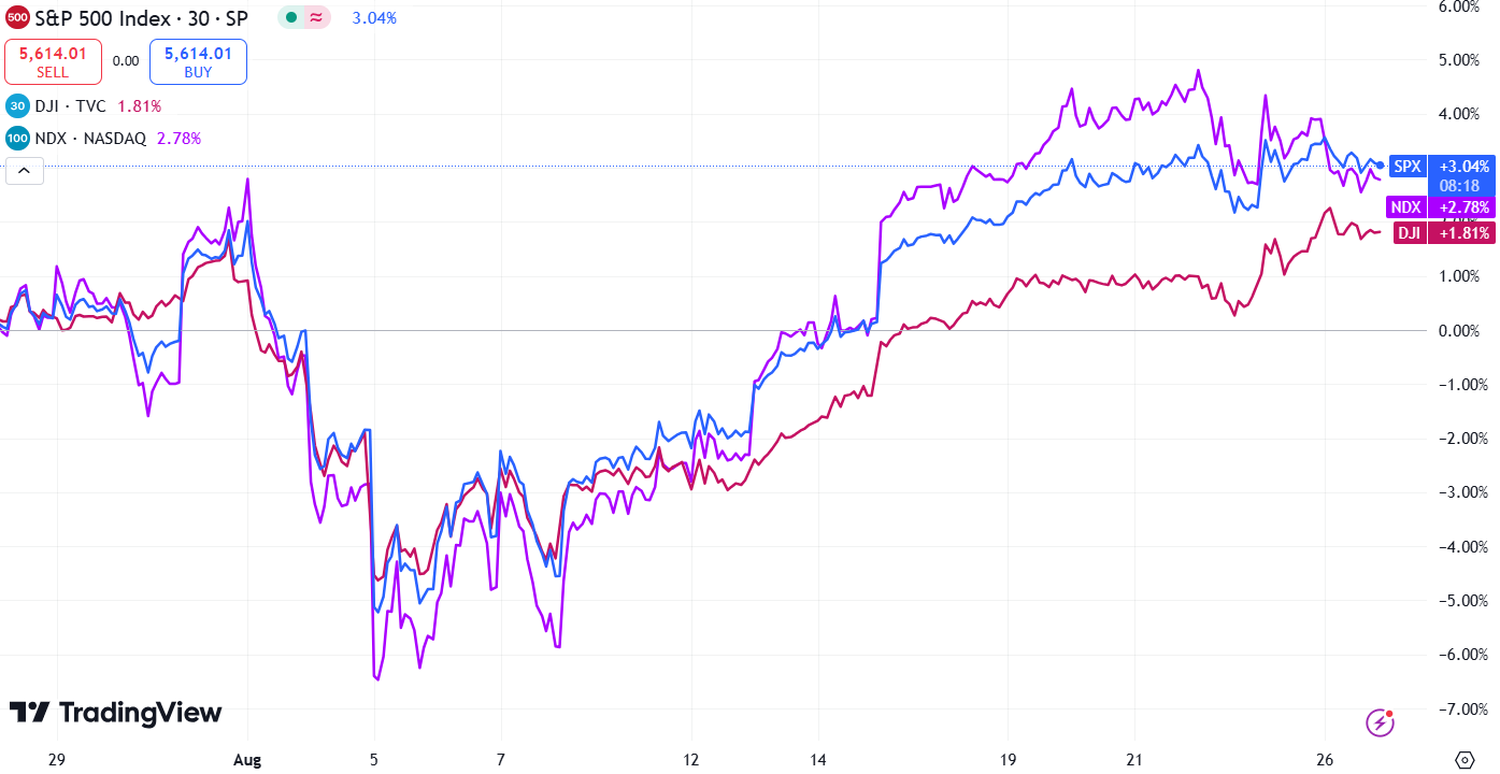

U.S. stock markets experienced mixed performance on Monday, characterized by choppy trading as investors braced for potential interest rate cuts and a highly anticipated earnings report from Nvidia (NVDA). Shares of the prominent AI chip manufacturer declined, dragging down other semiconductor stocks.

The Dow Jones Industrial Average (^DJI) managed to stay slightly above the flatline after briefly reaching an intraday high. Meanwhile, the S&P 500 (^GSPC) dropped by 0.3%, and the Nasdaq Composite (^IXIC), which is heavily weighted towards technology stocks, fell by approximately 0.7%.

The technology sector underperformed during the session, with notable declines in semiconductor giant Broadcom (AVGO) and electric vehicle maker Tesla (TSLA), both of which fell more than 3%.

Market Context: Anticipation of Fed Rate Cuts

The recent market movements follow a week of gains fueled by comments from Federal Reserve Chair Jerome Powell, who signaled readiness to pivot towards lowering interest rates in September. As a result, major indexes all recorded gains of more than 1% last week.

Market participants are now pricing in a series of rate cuts totaling 1% by the end of 2024. However, with only three Federal Reserve meetings remaining in the year—scheduled for September, November, and December—and critical data such as the August jobs report still pending, there is considerable uncertainty over the timing and scale of potential rate cuts. Wall Street is speculating on whether an initial 0.5% rate cut could be implemented.

Nvidia's Earnings: A Crucial Indicator for Market Sentiment

Investor focus is now firmly on Nvidia’s upcoming earnings report, set for release on Wednesday. As the marquee event of the week, Nvidia's results will likely influence broader market sentiment. Should Nvidia fail to meet the high expectations set by analysts, it could dampen the enthusiasm for AI-related stocks, which have been a significant driver of recent market gains, and challenge the market's recovery from August lows.

Additionally, investors are awaiting key economic data later in the week, including a report on the Federal Reserve's preferred inflation gauge, the Personal Consumption Expenditures (PCE) index, on Friday, which will provide further insight into inflation trends and potential rate-path decisions. Thursday's reading on the second quarter GDP will also be closely watched.

Oil Prices Surge Amid Geopolitical Tensions

Meanwhile, oil prices saw a significant uptick, rising around 3% due to reports of production shutdowns in Libya and escalating tensions in the Middle East following strikes by Israel and Hezbollah. Global benchmark Brent crude futures increased to $80.08 per barrel, while U.S. benchmark West Texas Intermediate (WTI) crude futures traded at $77.19 per barrel.

Historical Perspective: Implications of Aggressive Fed Rate Cuts

With Federal Reserve Chair Jerome Powell hinting at the beginning of a rate-cutting cycle, economists suggest that the depth of these cuts in 2024 will largely depend on the health of the labor market. Should the upcoming August jobs report, scheduled for release on September 6, confirm that the labor market is not as weak as the July report suggested, the Fed may opt for a modest 25 basis point cut rather than more aggressive measures.

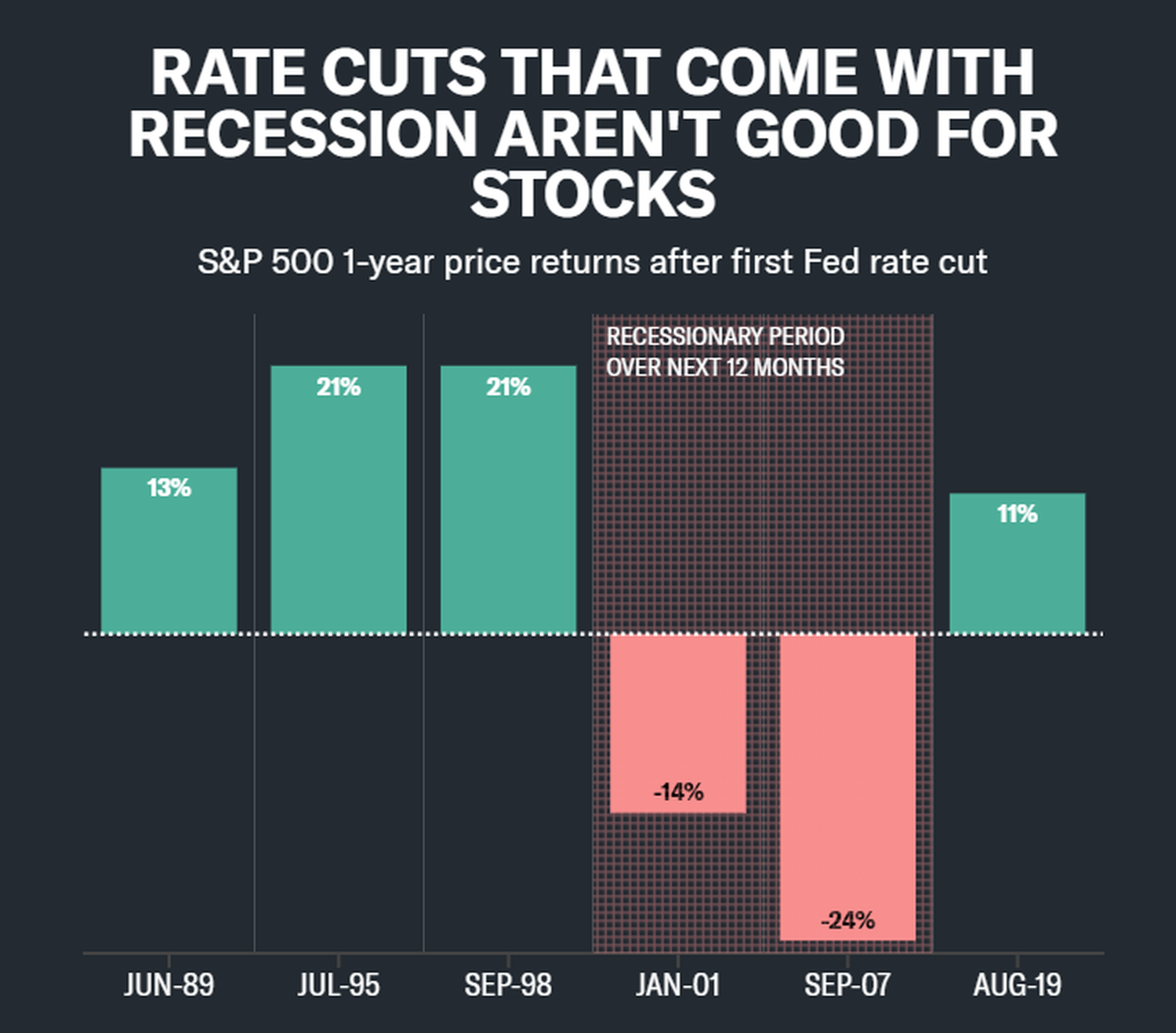

Historically, aggressive rate cuts driven by economic weakness have not boded well for the stock market. Research from Truist Co-CIO Keith Lerner indicates that since 1989, the S&P 500 has generally risen by at least 11% a year after the first Fed rate cut, provided the economy remained stable. Conversely, when the U.S. economy entered a recession within 12 months of the rate cut, the S&P 500 fell by at least 14% over the following year.

Nvidia’s Q2 Earnings: A Major Test for the AI Trade

Nvidia shares fell more than 2% on Monday, reflecting investor caution ahead of the company's earnings report on Wednesday. Nvidia’s performance will be a critical indicator for the tech sector, as investors look for signs that the AI-driven market enthusiasm can continue into the second half of the year.

Nvidia's stock has surged over 163% year-to-date and 60% in the last six months, underscoring its dominant position in the AI chip market. In contrast, shares of rival AMD (AMD) have risen 9% year-to-date but declined 14% over the past six months. Intel (INTC), meanwhile, has seen its shares plummet 57% since the beginning of the year and 53% over the last six months, as the company grapples with a challenging turnaround.

Stocks and Bonds: Returning to Historical Norms

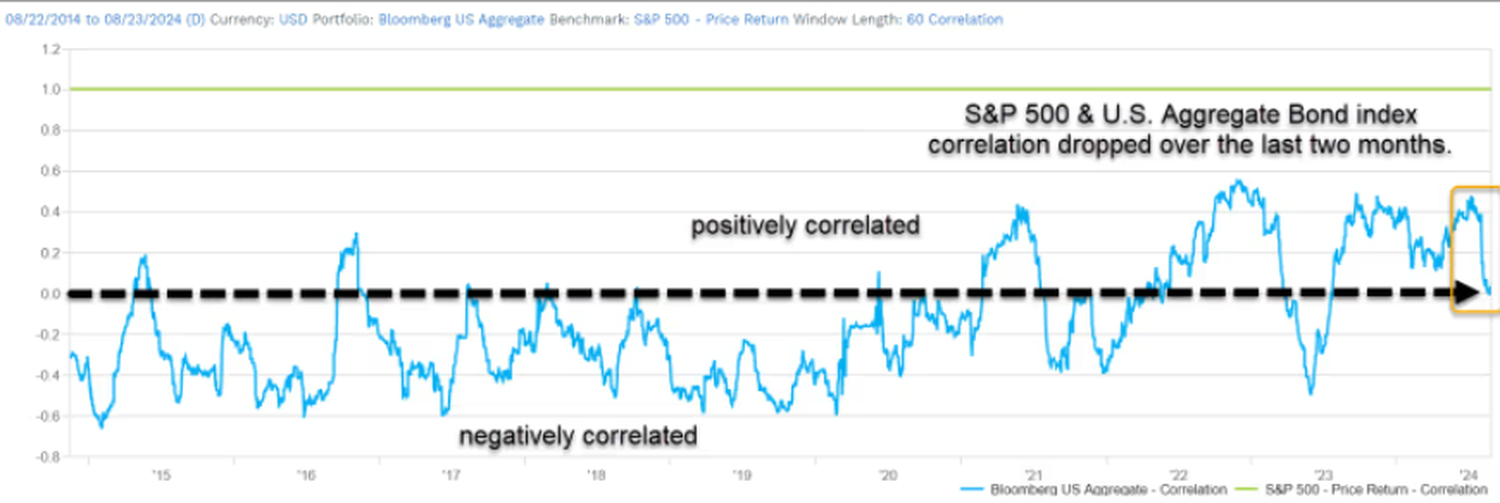

The traditional inverse relationship between stocks and bonds, which was disrupted by high inflation and low-interest rates, appears to be reasserting itself. Emily Roland and Matt Miskin, co-chief investment strategists at John Hancock Investment Management, have noted that the rolling 60-day correlation between the S&P 500 and the U.S. Aggregate Bond Index has been moving towards zero, signaling a return to normalcy.

Despite potential volatility ahead, the S&P 500's roughly 19.2% gain this year and the U.S. Aggregate Bond Index's nearly 3.6% advance are seen as positive developments, indicating that both asset classes are once again performing their traditional roles within diversified portfolios.

As the market navigates a complex landscape of economic data, geopolitical tensions, and corporate earnings, investors remain focused on key indicators that will shape the outlook for the remainder of 2024.