Sector Performance and Key Movers

Dow Gains Momentum as Cava and Health Stocks Tumble; Nvidia Turns Red

Technology Sector Notable Movements

Todays Summary: Stocks displayed mixed performance on Thursday afternoon, with the Dow Jones Industrial Average gaining traction while the S&P 500 held modest losses and the Nasdaq experienced a significant drop. Notably, Nvidia reversed its earlier gains, contributing to the technology sector's decline.

Market Overview

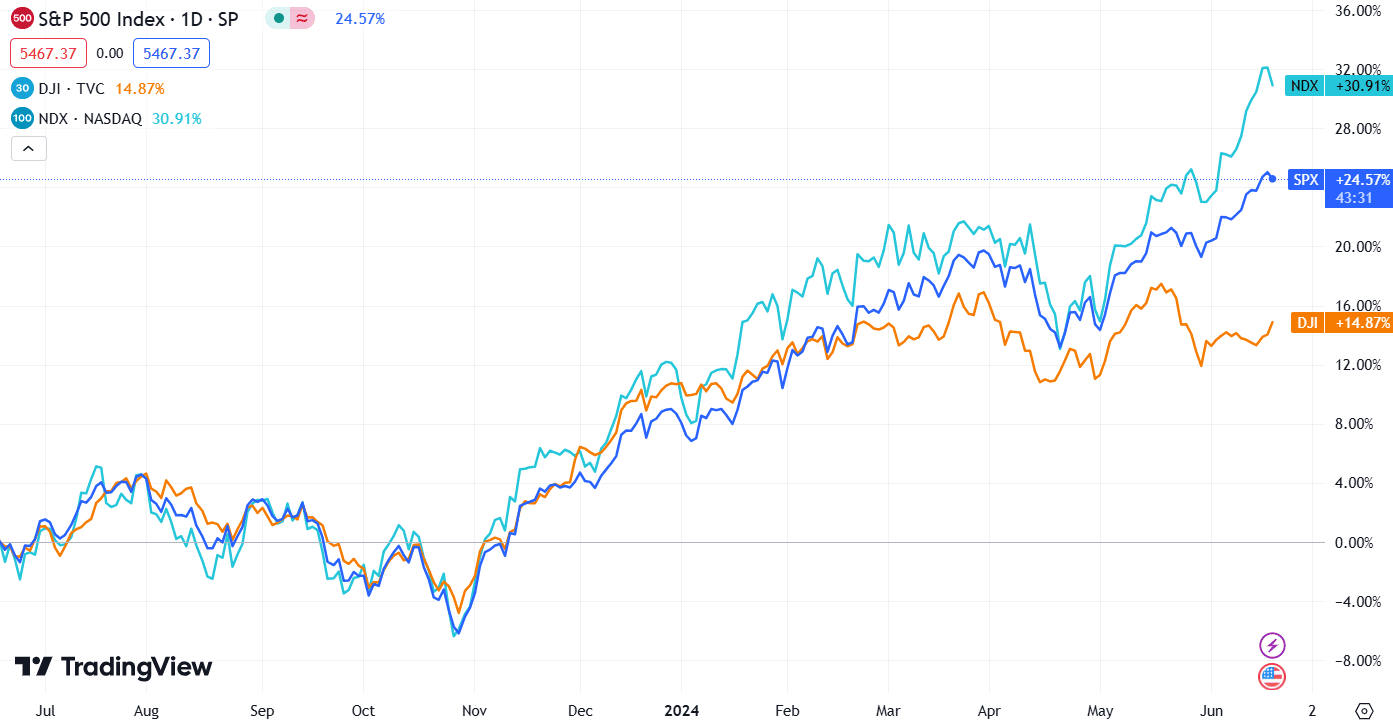

Dow Jones Industrial Average: The Dow rose 1%, maintaining support at its 50-day moving average, signaling strength and resilience in the blue-chip index.

S&P 500: The S&P 500 trimmed its losses to 0.2%, briefly touching the 5,500 level for the first time before pulling back. This marks a critical juncture for the index as it consolidates gains.

Nasdaq Composite: The Nasdaq fell 0.8%, driven by a sudden slip in the technology sector. Nvidia, after reaching a new high, reversed course and sank over 2%, contributing to the decline.

Russell 2000: The small-cap Russell 2000 weakened, dipping around 0.2% and remaining below its 50-day moving average, indicating ongoing pressure on smaller stocks.

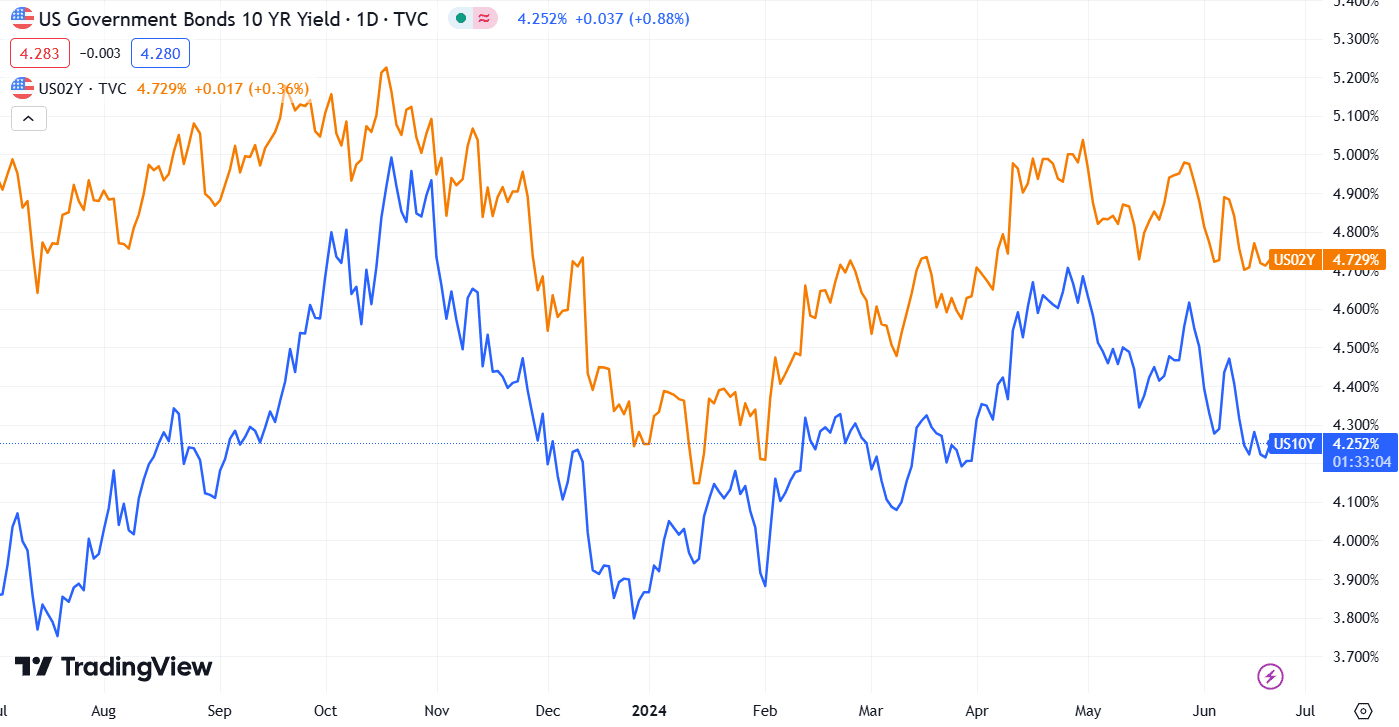

Treasury Yields: The 10-year Treasury yield added 4 basis points, reaching 4.25% after the release of new economic data, reflecting market reactions to the latest economic indicators.

Volume and Trading Activity

Volume increased on both the Nasdaq and the New York Stock Exchange compared to Tuesday, reflecting heightened trading activity. U.S. financial markets were closed on Wednesday in observance of the Juneteenth holiday.

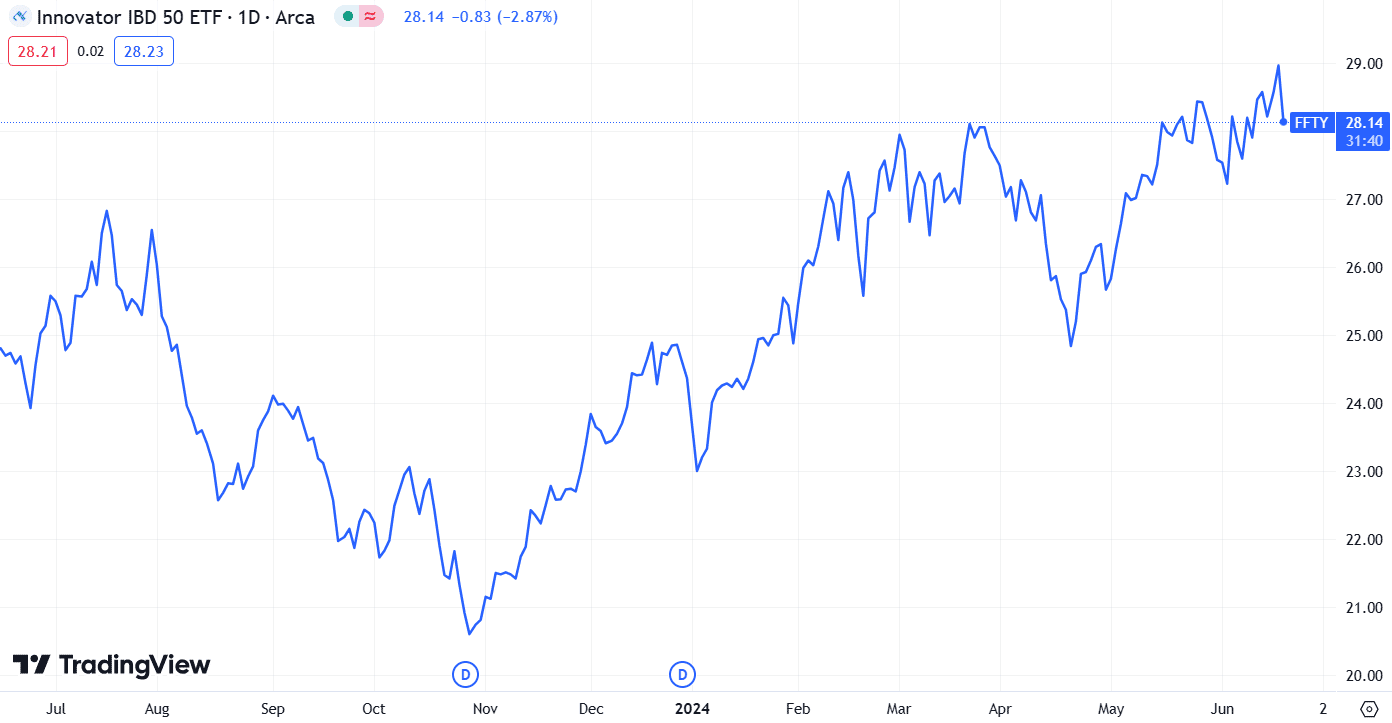

The Innovator IBD 50 ETF deteriorated, sinking 2.3%. Shares fell from the 5% buy zone of a cup base with a 28.35 buy point, hovering just below the entry point, signaling potential consolidation.

Sector Performance and Key Movers

Healthcare Sector:

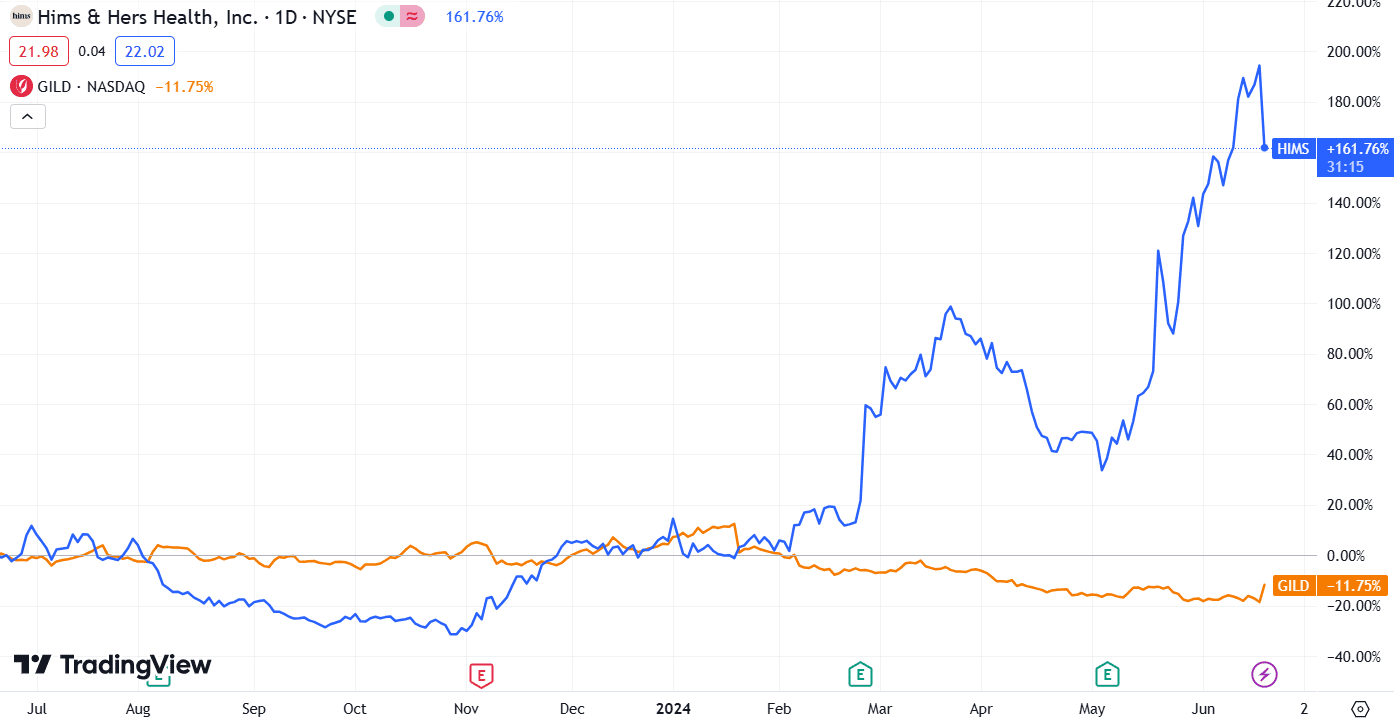

- Hims & Hers Health (HIMS): The telehealth provider tumbled around 10% after reaching a new high on Tuesday. Despite reporting better-than-expected first-quarter earnings and sales, the stock faced significant profit-taking. Its injectable weight-loss drug, GLP-1, announced for its telehealth platform, had earlier propelled the stock to a 155% gain year-to-date.

- Gilead Sciences (GILD): The biotech giant surged over 9% following positive news about its HIV treatment, reclaiming its 50-day line and becoming the top gainer on the S&P 500.

Restaurant Sector:

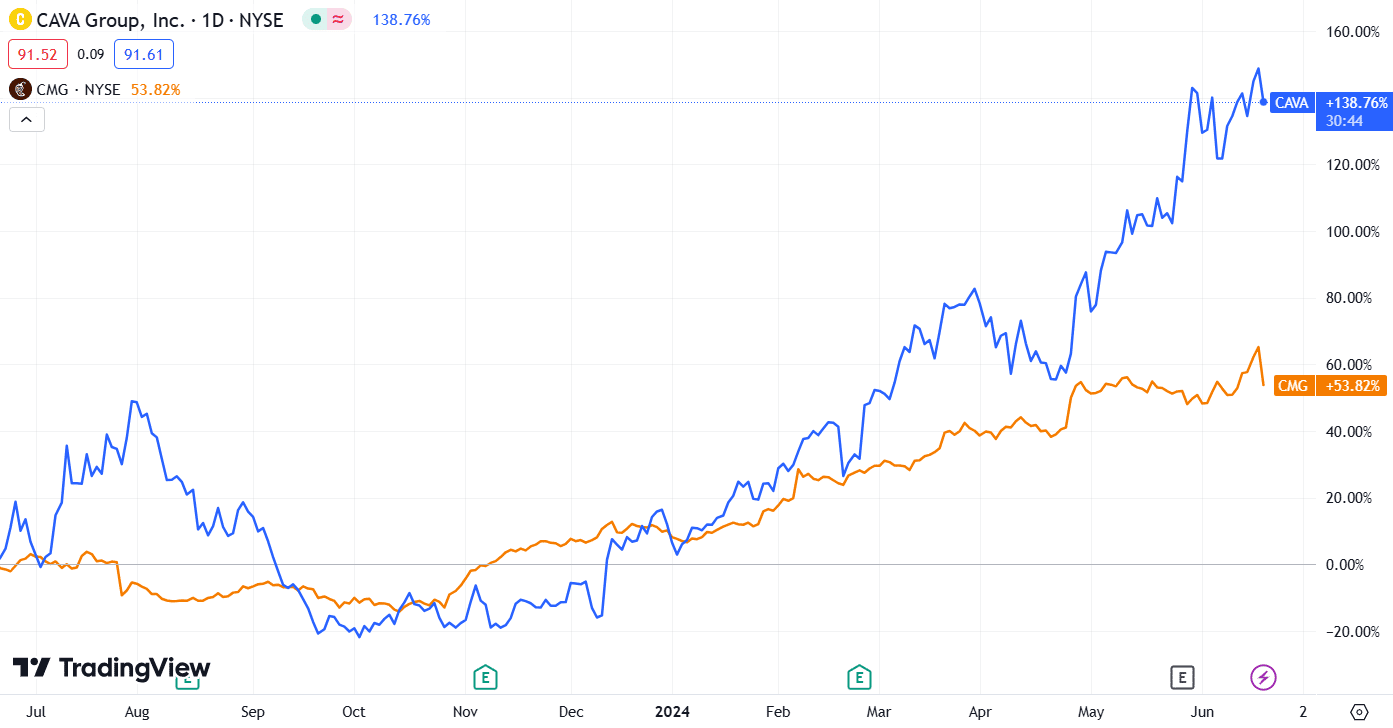

- Cava Group (CAVA): The Mediterranean fast-casual restaurant stock slid more than 3% after reaching a record high. Despite a strong year-to-date performance, shares pulled back, reflecting possible profit-taking.

- Chipotle Mexican Grill (CMG): The stock tumbled around 6% in heavy volume after hitting a record high on Tuesday. It remains extended from a cup base breakout in November but is now testing its 21-day exponential moving average.

Technology Sector:

- Nvidia (NVDA): Nvidia reversed lower after reaching another all-time high. Despite a remarkable year-to-date performance, the stock faced selling pressure, closing with a market cap greater than Microsoft for the first time on Tuesday. Tigress Financial raised its price target to 170 from 95, maintaining a buy rating.

- SPDR Technology Select Sector Fund (XLK): The ETF pulled back after 12 gains in the past 13 days, dropping 0.5%. Key holdings like Apple, Microsoft, Qualcomm, and Broadcom saw declines, with Qualcomm plunging around 4%.

Other Notable Movements:

- Super Micro Computer (SMCI) and Dell Technologies (DELL): Both stocks jumped following a tweet from Tesla CEO Elon Musk confirming the use of their server infrastructure for his startup xAI. Super Micro briefly topped the 1,000 level, forming a large cup base with a 1,229 buy point.

- Darden Restaurants (DRI): The parent company of Olive Garden gained after beating adjusted fiscal fourth-quarter earnings but missing sales estimates, reclaiming its 200-day line before pulling back.

Economic Data

Jobless Claims: Weekly initial jobless claims for the week ending June 15 were reported at 238,000, slightly above economists' expectations of 235,000 but below the revised 243,000 from the prior week. This figure remains near a 10-month high, indicating some softness in the labor market.

Housing Starts and Permits: The annual rate of housing starts in May was 1.277 million, below the forecast of 1.373 million and the revised April figure of 1.352 million. Annualized housing permits for May also fell short of expectations, coming in at 1.386 million versus the forecast of 1.45 million.

Crude Oil Prices: U.S. crude oil prices rose 0.9% to $82.31 a barrel, extending a rebound observed in June, signaling strength in the energy market.

Conclusion

The mixed performance across major indices underscores the ongoing volatility and sector-specific dynamics within the market. Investors are navigating a landscape marked by strong individual stock performances, sector rotations, and impactful economic data, necessitating a vigilant and adaptive approach.